The National Research Council of Canada Industrial Research Assistance Program (NRC-IRAP) and the CRA’s scientific research and experimental development tax credit (SR&ED) are two programs of major importance for Canadian innovators.

In this article, we will examine the key similarities and differences between SR&ED and IRAP and how these programs can work together to maximize your government funding for your innovative technology project.

Nature & Timing of Funding

The first fundamental difference between SR&ED and IRAP is that the former is a tax credit, while the latter is a grant. This mainly affects when the funding is received from each program, but also the administrative overhead necessary to access funds, as well as the reporting requirements that come with the funding.

A tax credit – like SR&ED – provides funding after the expenses are incurred. For Canadian Controlled Private Corporations, the SR&ED program offers a refundable tax credit disbursed after the CRA receives the claim. Therefore, SR&ED is typically less useful in cases when a business is looking to sustain their cash flow as they undertake a project.

This is especially true when a business submits their first SR&ED claim, since the retroactive funding will not arrive until after the end of the fiscal year. However, when claiming SR&ED every year, the refund from the previous year helps sustain the cash flow for the next period.

IRAP, on the other hand, requires monthly refund requests after the initial application is received and accepted. This means that a grant program such as IRAP is naturally more apt at sustaining a business’ cash flow while a specific project requires it. This is especially true for first-time applicants.

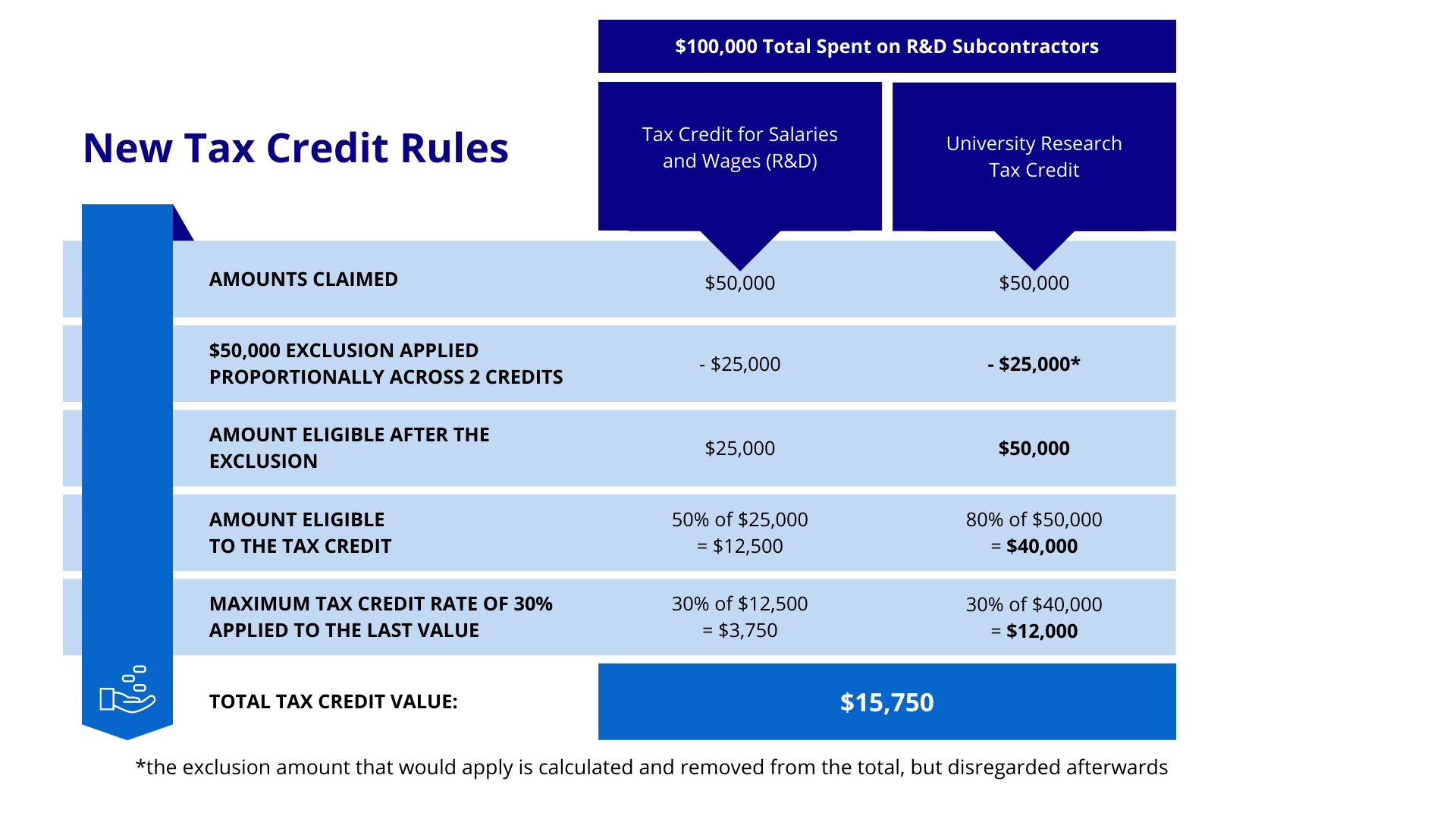

Funding Amounts

Once the federal and provincial tax credits are combined, SR&ED typically offers a refundable tax credit ranging from 54% (no provincial tax credit) to 74% (Quebec, beyond the threshold) of eligible salary expenditures to Canadian controlled private corporations. The exact tax credit rate depends on the size of the claimant company and a few other factors.

IRAP on the other hand is a grant and its funding is allocated on a discretionary basis. A certain amount is approved with the initial application when a budget is submitted. Therefore, the final funding amount will vary depending on the project, but typically goes up to 80% of salaries expenditures.

Eligible Expenses

IRAP and SR&ED share salaries as eligible expenditures, but treat them very differently. Since IRAP is a grant program and must be applied for before the project starts, applicants submit a budget which will end up dictating the amounts of funding they are entitled to receive, if accepted into the program.

For example, ABC Corp plans to assign 2 employees to work on a project they wish to fund through IRAP. They include this in their application, and the NRC agrees to fund up to 50% of those 2 employees’ salaries. Three months later, they realize they will need an additional team member to complete the project. The additional employee who ends up working on the project will, in this example, not be covered by the initial agreement, and therefore, their salary will have to be paid by ABC Corp, with no additional support from the NRC.

Since SR&ED is a refundable tax credit, it is able to account for all the actual costs incurred for a given project for the past fiscal year. Those costs are eligible salaries, subcontracting expenses, and other eligible expenditures related to eligible R&D activities for the SR&ED project. This may also include certain overhead expenses.

This level of specificity is why time tracking is important for a company planning to claim SR&ED.

Let’s consider ABC Corp again. Say they decide to forego IRAP funding altogether for simplicity’s sake – we will return to stacking IRAP & SR&ED later. They decide to attempt to claim SR&ED for their project at the end of the year instead and are tracking their employees’ time as it is spent on different tasks and projects.

We will assume, for simplicity sake, that ABC Corp is eligible for the maximum 74% refundable credit and have 5 employees in total. 2 of them begin working on the SR&ED project, but at some point during the year a third employee joins the project. When the time comes to submit the SR&ED claim, their eligible expenses would be as follows, assuming they did not receive any other overlapping funding for the project:

First, because they did not work on the R&D project at all, 0% of the salary of the 2 employees who did not do any experimental development work would be eligible for SR&ED.

For the 3 remaining employees who did do eligible experimental development work, the amount of time spent on the project needs to be taken into account in order to determine which portion of their salary is eligible for SR&ED.

According to their timesheets, at the end of the year it can be concluded that:

- Employee #1 worked on eligible experimental development work 75% of their time.

- Employee #2 worked on eligible experimental development work 50% of their time.

- Employee #3, who joined the project much later, worked on eligible experimental development work 25% of their time.

Therefore:

- 75% of Employee #1’s salary for the claim year is eligible for a 74% refundable tax credit.

- 50% of Employee #2’s salary for the claim year is eligible for a 74% refundable tax credit.

- 25% of Employee #3’s salary for the claim year is eligible for a 74% refundable tax credit.

Of course, SR&ED claims are never this straightforward, but this example seeks to illustrate the basic principles that guide how the eligible salaries are determined.

SR&ED can also fund materials necessary for the project, something IRAP does not do.

Evaluation Criteria

While there is some overlap when it comes to the eligibility criteria of SR&ED and IRAP, there are some important differences to note.

First, neither SR&ED nor IRAP have industry specific criteria – therefore, any company could theoretically be eligible as long as they are conducting eligible experimental development activities.

Experimental development can look drastically different depending on the industry. Find out how to determine if your project is eligible in our blog post all about the topic here.

This does not mean either program funds anything or everything. For example, IRAP excludes any clinical trial activities from their eligible project costs. This does not exclude pharmaceutical companies altogether but is still important to keep in mind when applying for funding.

Furthermore, neither program formally requires a minimum number of employees or years in business in order to be eligible. That said, while SR&ED can be claimed by an individual – there is no incorporation requirement – IRAP does require the company to be incorporated, and the company generally needs to be revenue-generating as well. Businesses with more than 500 employees are not eligible for IRAP, as the program is purposed to support small and medium businesses.

While IRAP does not require a minimum number of employees, the program’s monthly reporting requirements make it more complicated to handle for small businesses with little administrative staff. A business entirely run by its two co-founders or an otherwise very small, specialized technical staff are rarely awarded IRAP funding. Therefore, the size of the team does have an impact on the usefulness of IRAP to a specific company.

SR&ED is usually more advantageous for such smaller teams because, while it requires diligent time tracking of all activities related to the project throughout the year, the claim is only submitted once for the whole year.

A key difference to note between SR&ED and IRAP’s evaluation criteria is that the CRA has no return-on-investment considerations when they fund a SR&ED project. On the other hand, IRAP’s mission is to advance technology in Canada and stimulate Canada’s growth as a science and technology leader on the world stage. Therefore, eligible projects are selected much like investments. Only those with the greatest commercialization potential and that advance science and technology in a way that the NRC considers significant enough will receive funding. In this way, NRC IRAP is a competitive program – not all applicants, even if they may be eligible, receive funding.

SR&ED is not subjective. As long as a project and related corporation/individual meet the criteria according to the law, it will be accepted – assuming the claim is submitted correctly and on time.

Stacking

It is perfectly possible for a company to benefit from both SR&ED and IRAP for the same project. However, a few things must be kept in mind.

Since some eligible expenses could both be covered by SR&ED and IRAP, having received IRAP funds throughout the project would necessarily reduce the amount of the future SR&ED refund. Of course, the difference here is the timing of when the funds are received. As mentioned earlier, IRAP is better designed for supporting cash flow because of its monthly reimbursement structure, so it makes sense to apply for IRAP if increasing cash flow during the project is a primary concern. It will still be possible to submit a SR&ED claim and receive the refundable tax credit amount, but it will almost certainly be reduced by the amounts that overlap with NRC IRAP funded activities.

Want to find out more about the best practices related to stacking funding programs? Read our dedicated blog post here.

Stacking funding programs requires paying extra attention to the stacking limits of each program and how they interact with each other. Double-dipping – covering the same expense twice – can come with its fair share of trouble.

This is particularly true when using IRAP as the NRC conducts a systematic audit of every application, whereas SR&ED claims do not automatically get audited.

Have questions about the SR&ED audit process and how to prepare for it? Find out more here.

Whether you get audited or not, you should always be ready by preparing your claim carefully and having all the necessary documentation.

Disclaimer: This article is intended for informational purposes only and does not constitute professional advice.

To know more about SR&ED, IRAP and any other funding program and how your business can benefit from it, contact Mike Lee at: 1-800-500-7733, 110 mlee@rdpartners.com.